You know how the rules sometimes shift quietly in the background, and most people don’t notice until the year is already half over? That’s exactly what’s happening with the 401(k) in 2026. A 401(k) is a workplace retirement plan that lets employees save money from their paycheck before taxes. Many employers also match part of the contribution, which helps the account grow faster over time. The Internal Revenue Service (IRS) is raising contribution limits, adjusting the numbers, and opening more room for tax-advantaged savings. If you don’t pay attention early, that extra space slips away, and once the year closes, there’s no way to get it back.

A lot of people treat their retirement account like something that runs on autopilot, but this is one of those updates where checking your settings ahead of time actually changes your outcome. The limit goes up, but the benefit only helps if you adjust your contribution before the year gets too far along.

So before the new rules take effect, let’s walk through what’s changing and what you can do now to stay ahead without adding stress.

What’s Changing in 2026?

The Core Limit Increases

The IRS is increasing 401(k) contribution limits for 2026, and the change is larger than the typical annual bump. These updates tie back to inflation patterns, broader retirement policy, and cost-of-living adjustments. Even if the numbers themselves look simple, they shape your entire year of tax-advantaged saving.

You’ll be allowed to save more than before, both through the standard contribution limit and the catch-up amount for older savers. That means more money sits in your account, grows tax-deferred, and builds momentum over time.

How do Employers Apply the New Numbers?

Where many people run into trouble is assuming that the new limits automatically update through payroll. Some workplaces use payroll services, HRMS, and HR software tools that handle contribution increases automatically at the start of the year. Others require manual updates.

Even in companies that rely heavily on integrated HR systems and workforce analytics, updates don’t always roll out at the same time. For example, systems that handle onboarding, benefits, tax forms, or background verification of employment may update quickly, while contribution settings may lag behind.

That’s why it’s important to check your contribution rate directly when the new year begins; waiting until mid-year can cost you valuable tax-advantaged savings.

How do the New Limits Affect Your Savings?

More Room to Grow

The higher limit gives your account more space to grow without yearly taxes reducing your long-term balance. Every extra dollar saved before taxes has more years to compound.

Dependence on Workplace Systems

The impact of the new limits depends on how your employer handles updates. Some companies rely on HRMS, payroll services, workforce analytics, or updated HR software that automatically adjusts contribution amounts. Others require employees to log in and update their own settings. A quick check early in the year can help you avoid months of under-saving simply because an update didn’t go through.

Long-Term Growth Advantages

Even a small

l increase in annual savings makes a difference. If your updated contribution starts early, you get more pay periods working in your favor, which strengthens your retirement plan over time.

A More Predictable Budget

As the limit increases, you can spread your contributions more evenly throughout the year. That means less stress at the end of the year and more balanced cash flow throughout the year.

With the new limits in place, you can build a steadier, more controlled retirement strategy without needing major lifestyle changes.

Why 2026 Is a Critical Year for 401(k) Savers

A Bigger Shift Than Usual

Planning for retirement always works better when you understand the rules before they change, and 2026 is shaping up to be one of those years where the IRS adjustment truly matters. These new contribution limits affect how much you can put aside before taxes and how quickly you can grow your account.

Most people don’t check retirement updates often, and that’s completely normal. Life moves quickly, work piles up, and even big companies rely on tools like workforce analytics, HRMS, and HR software just to keep up with their own policies and employee changes. Savers can take a cue from that approach. The 2026 limit increase gives you an opportunity, but only if you prepare early.

How Early Awareness Helps

When the contribution limits rise, you get more room for tax-free compounding. More space for your money to grow without taking a yearly tax hit. If you wait until late in the year to adjust your contribution, part of that expanded space stays unused. And once December passes, it’s gone.

That’s why 2026 matters. It’s not just another update; it’s a meaningful expansion. The people who understand it ahead of time and adjust early are the ones who collect the full benefit.

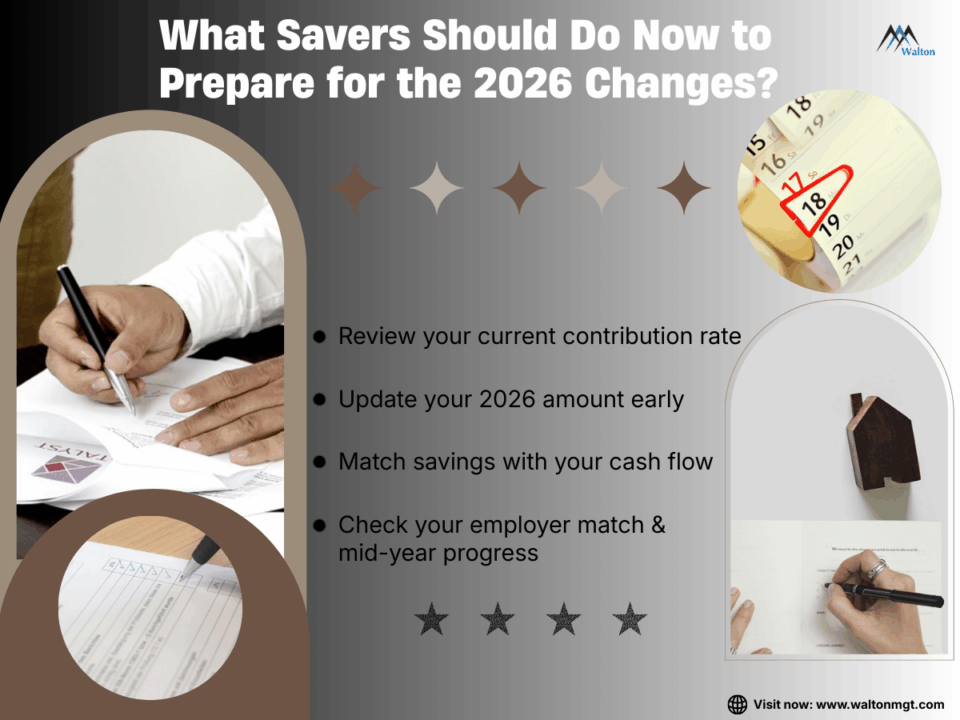

What Savers Should Do Now to Prepare for the 2026 Changes?

Step 1: Review your current savings rate

Look at your month-to-month contribution amount and see how close you are to the current limit. Even a modest increase spread over twelve months helps you use the 2026 space without feeling financial pressure.

Step 2: Update Your Contribution Early

Many workplaces use integrated HR systems that manage everything from onboarding to background verification of employment and internal workflows. These systems handle many tasks efficiently, but contribution updates don’t always happen automatically. Reviewing your settings at the start of the year ensures the new 2026 number actually applies.

Step 3: Match Your Contribution to Your Cash Flow

Some people prefer increasing their contribution slowly throughout the year. Others make a one-time update at the start. Both approaches work, as long as you stay consistent.

Step 4: Check Your Employer Match Rules

If you raise your contribution too quickly and hit the limit early, your employer match may stop early, too. A steady pace ensures you collect the full match throughout the year.

Step 5: Review your progress halfway through the year

A simple mid-year check helps you confirm your updates were processed correctly through payroll services, HRMS, or hr software tools. This prevents surprises in the fall when adjustment time is limited.

By taking these steps ahead of time, the 2026 transition becomes much smoother, and you’re less likely to miss valuable tax-free space.

Tips for High Earners Under the New Rules

High earners often face unique challenges with contribution timing. When you reach the limit early, you miss employer matching, and you lose part of the advantage the new 2026 rules offer.

Review Your Contribution Pace

If you usually hit the limit by summer, spreading contributions more evenly across the year helps you maximize your employer match. Most workplaces rely on payroll services or HRMS that automatically pause contributions once you hit the cap. Adjusting your pace ensures you don’t miss anything.

Plan Around Bonuses

Large bonuses can push you closer to the limit faster than expected. Adjusting your contribution rate before the bonus arrives helps you avoid maxing out too early.

Learn From Employer Tools

Some companies use workforce analytics, hr software, and tools like ForeSite to study compensation patterns. These same tools give employees insight into how bonuses, overtime, or commission patterns affect savings timing.

Maximize the New Space

The updated limits are good for high earners, but the benefit really shows when your timing is deliberate. A few small adjustments can help you use the full higher limit.

Mistakes to Avoid

Main Points

- Not checking the 2026 limits early

- Keeping last year’s contribution rate

- Assuming HR updated everything

- Hitting the cap too early and losing the employer match

- Letting bonuses push you over the limit

- Waiting until the end of the year to adjust

- Not reviewing how HR software tools apply your updates.

Many savers walk into the new year with old settings, and that keeps them from using the full 2026 space. Some assume HR automatically updated everything, even though HRMS, hr software, and payroll services don’t always adjust retirement settings on their own. Bonus timing can also push contributions up faster than expected. Checking everything early keeps your savings plan stable and helps you use the full benefit of the updated rules.

Final Action Checklist

Start with the basics

Compare the new limits with your current rate so you know where you stand.

Update early

Make adjustments at the beginning of the year so your company’s payroll services, HRMS, and hr software tools can process changes correctly.

Review employer match rules.

Make sure you aren’t hitting the limit too early and missing out on part of your employer’s matching contribution.

Consider bonus timing

If you expect a bonus, plan your contribution percentage around it so it doesn’t push you over the limit ahead of schedule.

Look halfway through the year.

A mid-year check keeps everything on track, especially in workplaces that use connected HR systems for onboarding, benefits, and tax updates.

Conclusion

The 2026 401(k) updates are easier to manage when you make a few early adjustments and stay aware of how your workplace systems handle the changes. Reviewing your contribution settings, checking how HRMS, payroll services, and hr software apply updates, and pacing your savings around income shifts helps you use the full benefit of the higher limits. And if any part of the process feels unclear, you can always contact us so we can walk you through it step by step.

Companies rely on tools like workforce analytics, hr software tools, ForeSite, and even programs tied to the work opportunity tax credit, tax credit for hiring veterans, and handling an unemployment insurance claim to stay organized. A simple check-in on your own savings plan works the same way.